IFAC’s research suggests that PE investment has the potential to set a higher standard among accountancy firms for their operational efficiency, service offerings, and competition for clients. Meeting this challenge may mean more Firms will seek PE investment—across all sizes of accountancy practices—leading to a reduction in number of Firms, but leading to larger and better resourced Firms.

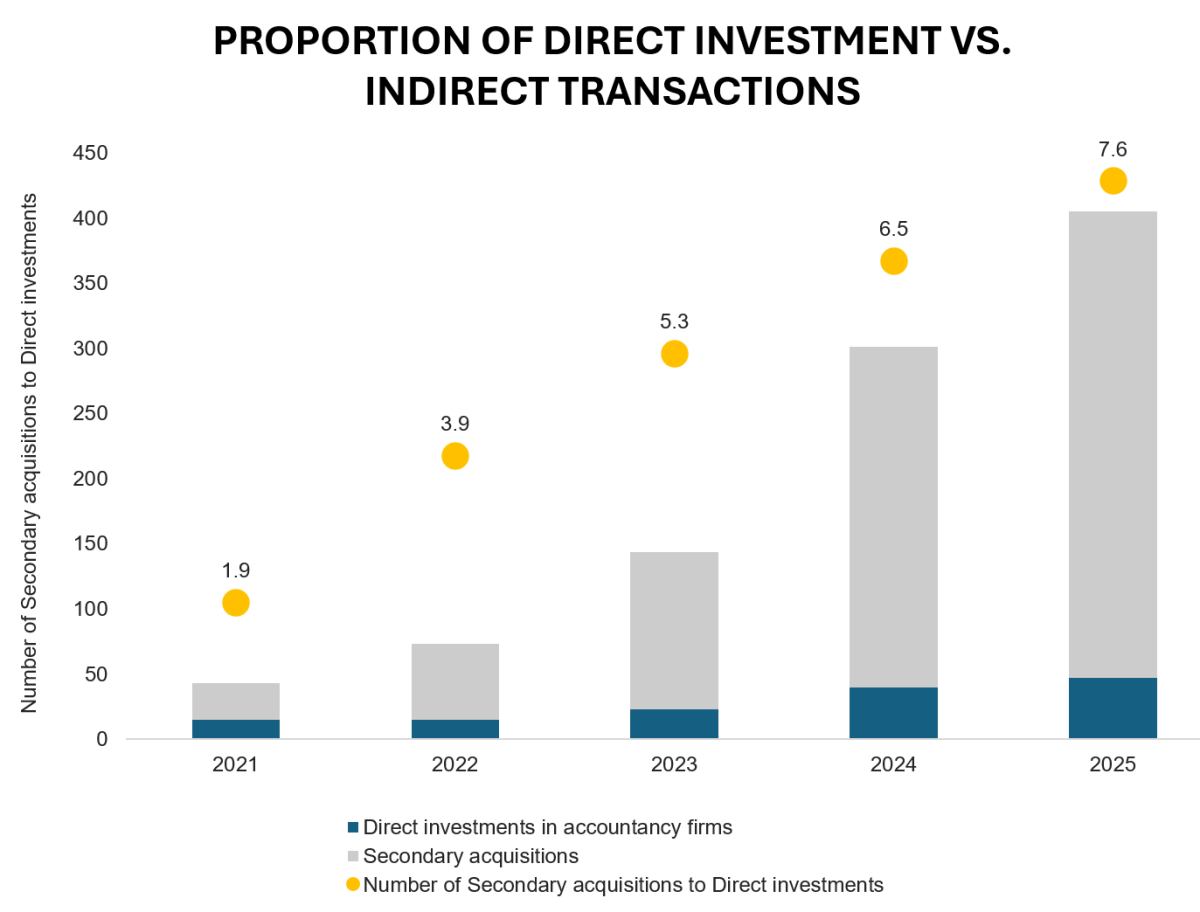

The graphic below illustrates this consolidation. Over the last five years, an increasing number of direct PE investments in accountancy firms has led to a dramatically higher number of indirect or subsequent “roll-up” transactions. As of year-end 2025, less than 200 direct investments facilitated nearly 900 subsequent transactions—typically rolling up smaller Firms into a larger, lead / direct investment Firm. In 2025, each direct PE investment resulted in 7.6 additional transactions. This “consolidation index” has increased four-fold since 2021.

This data suggests that the structure of the market for accountancy services in jurisdictions where PE investment is prevalent (i.e., the UK/Ireland, U.S., and western Europe) is changing. Fewer, larger Firms in the future may introduce challenges, including higher fees for critical services like audit and tax advisory, but also potential opportunities from enhanced service offerings from larger and better resourced Firms and a more competitive environment for winning client engagements.

-

Potential Challenges and Risks

PE-driven acquisitions, mergers and consolidation will result in fewer Firms. A reduced number of Firms charging higher fees for audit and advisory services will impact all clients, but especially SMPs and their SME clients.

PE-backed Firms may re-assess their existing audit clients—dropping those that are larger, higher-profile, and higher risk in favor of more mid-tier clients (i.e., those subject to lighter regulatory oversight). Firms with insufficient market share in specific industries or in public interest entity (PIE) or stock exchange-traded audits may exit those markets. This dynamic could result in greater audit concentration, less client choice, and potentially higher fees for PIE and stock exchange-traded companies.

Commercial interests are likely to prioritize expanding advisory services, not audit and assurance. Therefore, PE investment may accelerate shifts in audit / assurance services away from smaller, less-profitable engagements—again, resulting in higher fees for audit services.

IFAC’s research highlights that direct PE investment drives multiple “indirect” or “roll-up” acquisitions, which can reduce the number of Firms remaining in professional associations and international networks. This consolidation may challenge the delivery of global service offerings from mid-tier Firm networks or associations.

Direct investments in accounting firms, as well as subsequent follow-on acquisitions, may introduce a more “corporate” and less client-centric environment and management style, which may not be a good match with existing clients or Firm employees—prompting defections (both clients and employees) from PE-backed Firms.

-

Potential Opportunities and Benefits

The accountancy profession is perhaps too fragmented in some jurisdictions—especially with respect to smaller firms—and could benefit from some consolidation into better resourced, more resilient, more sustainable accounting Firms that can meet client needs. In addition to accelerating consolidation through roll-up transactions, PE investment can also incentivize mergers among independent Firms who do not wish to accept PE capital but will benefit from pooling resources.

Larger, more resilient Firms—who pursue growth through advisory services—will offer a broader range of higher-quality, and more specialized services to clients.

A commercial focus on scale, revenue and growth may increase competition among PE-backed Firms for audit engagements, as well as drive expansion of non-audit/advisory services - which benefits clients.

PE investment is about scale and growth—so it seems very likely—and IFAC data demonstrates—there will be consolidation and fewer, larger accountancy firms in the future.