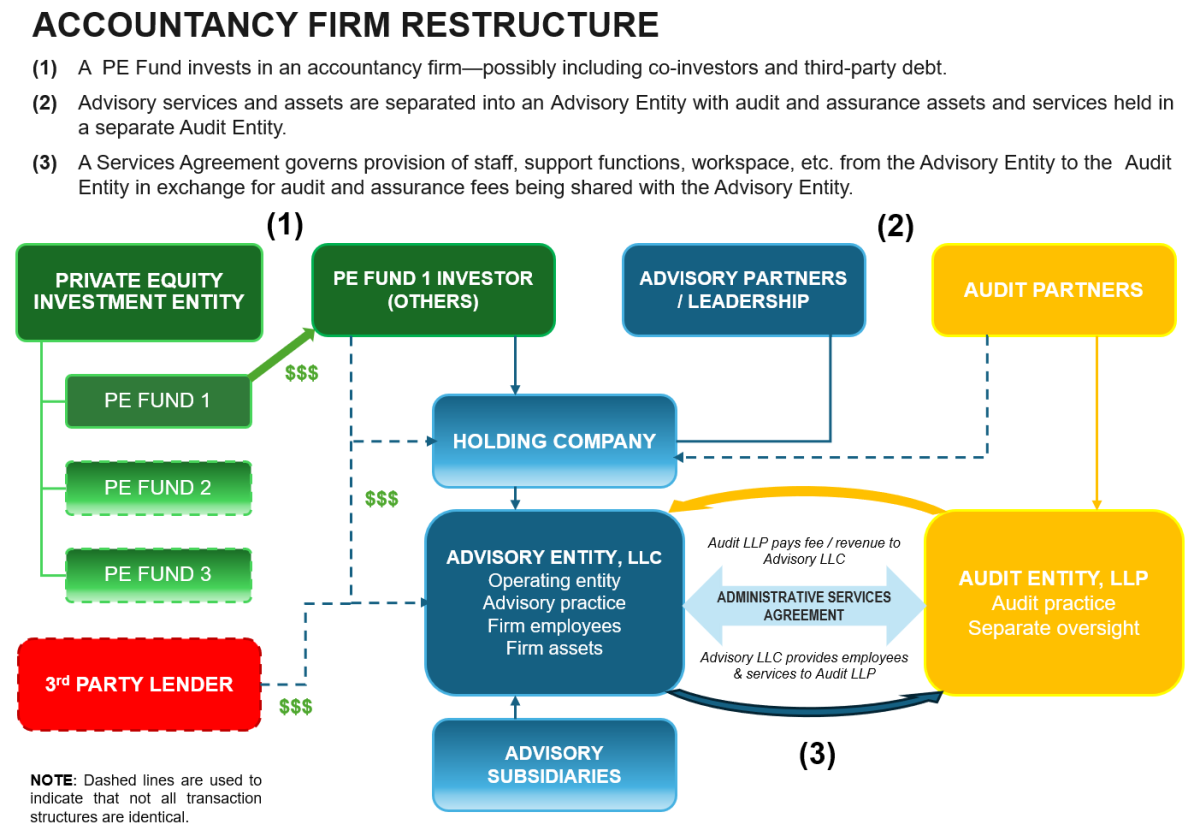

Firm Restructuring: When Private Equity invests in an accountancy firm that provides audit and assurance services, a restructuring (e.g., “Alternative Practice Structure” - “APS” in the U.S.) is typically required to maintain compliance with ownership restrictions that govern audit practices (i.e., imposed by local regulatory authorities, PAOs, or firm network rules). This restructuring typically happens at the time of initial investment by a PE fund, sometimes including additional co-investors. Capital is typically invested in the Advisory Entity or one or more Holding Companies (see step 1 below).

A new Advisory Entity is created—effectively separating advisory services from audit/assurance services, so that matters of independence, conflicts, and audit quality remain under the control of audit partners who direct assurance-related activities in a separate Audit Entity (see step 2 below). Future follow-on acquisitions can be consolidated into the Advisory Entity with acquired audit and assurance functions either consolidated into the Audit Entity or ringfenced in a separate partnership (i.e., also under audit partner ownership/oversight). Holding companies and subsidiaries may be used to satisfy third-party lender requirements, manage tax consequences, and address other legal matters.

A long-term contractual agreement between the Audit Entity and the new Advisory Entity—often called an Administrative Services Agreement (“ASA”)—is used to document terms and conditions that address staff, support services, workspace and other resources provided by the Advisory Entity to the Audit Entity. In exchange, some audit and assurance related fees/revenues are paid by the Audit Entity to the Advisory Entity. The ASA typically includes features to help ensure that matters of independence, conflicts of interest, and audit quality remain under the oversight and control of audit partners who direct audit/assurance-related activities (see step 3 below).

Significant Influence: Firms considering PE investment may encounter questions from regulators and other stakeholders about whether the APS approach and the associated ASA are a legal construct—“form over function” or “work around”—that does not sufficiently address the possibility of undue PE influence over both advisory and regulated assurance services. Structural features of the ASA, as well as Firm leadership’s commitment to implementing them in a manner that supports audit quality and independence, are key considerations in a PE investment transaction.

Secondary Sales: ASAs are typically structured to survive secondary sales, IPOs or other ownership changes—effectively defining future consolidated fees and revenues from the assurance and advisory operations. The detailed terms of this agreement help prospective investors place a valuation (typically expressed as a multiple of EBITDA for the advisory entity) on the holding that is under consideration to be sold by the current PE investor—either to another PE manager or other type of investor.

Leverage: Debt is often part of the capital provided by a PE investor—at the Advisory Entity level—increasing economic return on PE investment but potentially increasing pressure on the accountancy firm’s commercial performance. While PE investors are comfortable making leveraged investments, accountancy firm leadership needs to understand the degree of leverage, the details of debt covenants, and the underlying assumptions that support debt service obligations as part of the PE investment decision.

1. A well-structured Administrative Service Agreement is critical to maintaining an appropriate relationship between private interests and the public interest responsibilities of audit and assurance activities.

2. Firm leadership must take responsibility for and ensure that PE investment does not exert undue pressure on the fragile balance between commercial interest and public interest. Professionalism, integrity, and the public interest mindset of Firm leadership and audit partners must be maintained.