High-quality audits are essential to strong organizations, financial markets and economies. They depend on individuals, acting in the public interest, with experience, integrity, independence, professional judgement, and specialized skills. Audits must be conducted in an environment that attracts, develops, and retains the best talent while adhering to the highest ethical standards. [See IFACs Point of View: Achieving High Quality Audits.] The incidence of private equity capital investment in accountancy services since 2021 has prompted discussion among regulatory bodies, accounting firms, Professional Accountancy Organizations, and other stakeholders about the potential implications of PE investment on independence (see Independence Considerations and Implications) and overall audit quality.

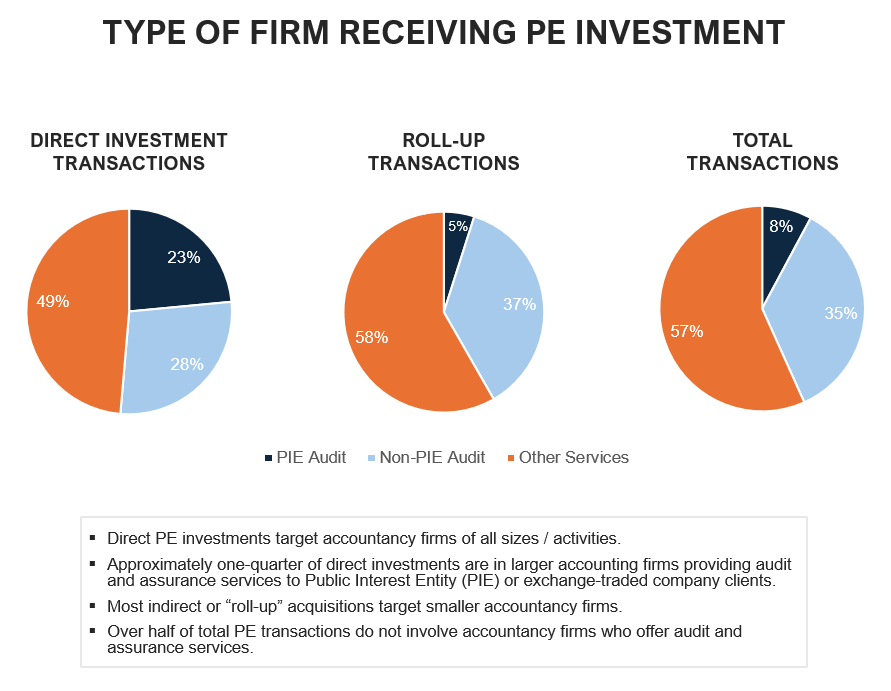

IFAC’s analysis of the potential impact of PE on audit quality starts with the data-driven observation that most PE investment in the accountancy services sector does not involve Firms providing audit or assurance services. According to our review of publicly available information, only about 25% of direct PE investment involves assurance practices servicing Public Interest Entities or stock exchange-traded companies. This percentage drops to under 10% for all transactions, including indirect or roll-up acquisitions.

In this context, IFAC still applies a risk-based approach—focusing on audit/assurance-related matters including independence, conflicts, audit quality, etc.—that we believe are primary concerns of regulators and other stakeholders and that have the greatest potential impact on public perception and trust in the profession. Our research and engagement have identified both challenges / risks to audit quality, as well as potential opportunities and benefits that can support, or even enhance, high quality audits, post PE investment. These factors may not be relevant to advisory-only practices.

-

Potential Challenges and Risks

The median holding period for PE buyout-backed investments is approximately five and a half years (see reference). This relatively short-term investment approach could create an overly commercial and profit-centric focus that can be an impediment to the longer-term investments and partnership culture that have historically supported and sustained high-quality audit practices.

The sale of a PE-backed Firm to a subsequent investor—at a significantly increased price-to-EBITDA multiple (e.g., Citrin Cooperman in 2025)—may limit additional investments in technology and other innovations necessary to support audit quality over time. This “leakage” of PE capital—to investors, Firm partners, etc.—may further increase commercial pressure and reduce support/resources supporting high-quality audits.

An undue focus on profitability may jeopardize quality management. For example, PE pressure to increase its return on investment may provide inappropriate incentives to audit leadership—potentially leading to concerns related to relaxed quality controls, identifying fewer potential errors, performing fewer procedures, allocating fewer staff hours, etc.

Especially in circumstances where PE investment is driving multiple acquisitions or consolidating / roll-up transactions, culture, procedures, and quality controls can vary between Firms and need to be harmonized—so audit quality may be inconsistent or susceptible to a “lowest common denominator” approach to implementation.

PE investors may conclude that they are legally insulated from audit failures or other assurance practice-related problems. For example, in a U.S. legal context, a Firm restructuring that establishes a separate Advisory Entity as a Limited Liability Company (“LLC”) typically protects PE sponsors, investors, and LLC Directors from liabilities arising from actions of the separate Audit Entity partnership. This legal protection may make audit quality seem less important.

PE investors often introduce new governance structures (at the Holding Company and/or Advisory Entity level) that are less “partner” and more “corporate director” in nature. Concerns exist that these restructurings can dilute or effectively reduce the influence of audit partners and their control/oversight of audit and assurance client selection and engagement performance.

-

Potential Opportunities and Benefits

PE investors understand the linkage between a Firm’s brand / reputation and audit quality. As PE investors seek to increase the value of their investment in a Firm(s), they will want to preserve, if not enhance, audit quality, as well as the quality of advisory service offerings. IFAC’s stakeholder engagement indicates that the investment thesis of most PE organizations is focused on Firms that demonstrate high performance, professionalization, and operational excellence—all of which should support audit quality.

A well-structured Administrative Services Agreement (see Transaction Structure Considerations) can include specific terms that provide audit partners with access to sufficient resources and staffing, as well as protect against inappropriate influence over issues like engagement budgets, audit staff compensation, and other matters necessary to support high-quality audits.

PE investors proport to offer Firms enhanced strategic analysis/vision, better management practices, new technology, better hiring and retention, and economies of scale that are driven by consolidation, shared administrative services, and standardized processes. All of these improvements should, on balance, enhance effectiveness, efficiency, and quality of both advisory and audit/assurance services.

PE investors who plan to realize gains after an initial hold period must think strategically and manage from the perspective of the next investor—be it another PE fund, pension plan, endowment, or other alternative asset class investor. Sustaining high-quality audit (and advisory) services is therefore important over both the short and longer-term time horizon.

1. Regardless of ownership, governance structures, or “culture,” Firms must maintain focus on the value of their brand and the accountancy professions’ unique value drivers—ethics, independence, technical expertise, client focus, regulatory oversight and public interest responsibility—all of which support audit quality.

2. Firms who are considering PE investment should make sure that potential PE investors appreciate the critical importance of high-quality work—both audit and advisory services. Increased focus on the commercial “business of accounting” cannot overtake the “profession of accounting.”

3. Best practices suggest Firms should review and update their quality management frameworks as appropriate, post PE investment.