In early April 2018, the IESBA released a completely rewritten and revamped Code of Ethics for professional accountants (PAs). Renamed “International Code of Ethics for Professional Accountants (including International Independence Standards) (“the Code” or “the revised and restructured Code”), the Code will become effective in June 2019. It packages all substantive advancements in ethics and independence over the last four years into a single document and includes the new provisions relating to non-compliance with law and regulations (“NOCLAR"), which are already effective since July 2017, and the revised independence provisions relating to long association which comes into effect in December 2018.

Key Areas of Focus

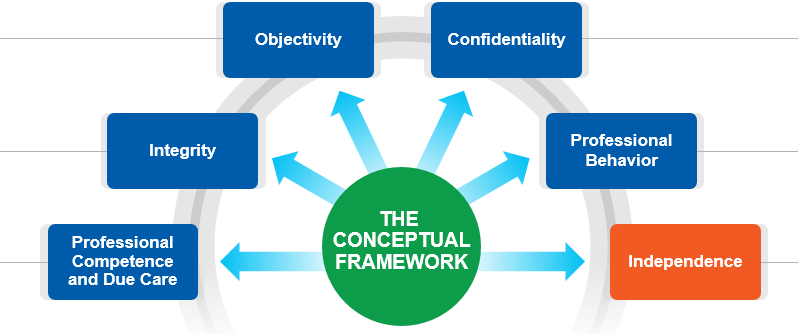

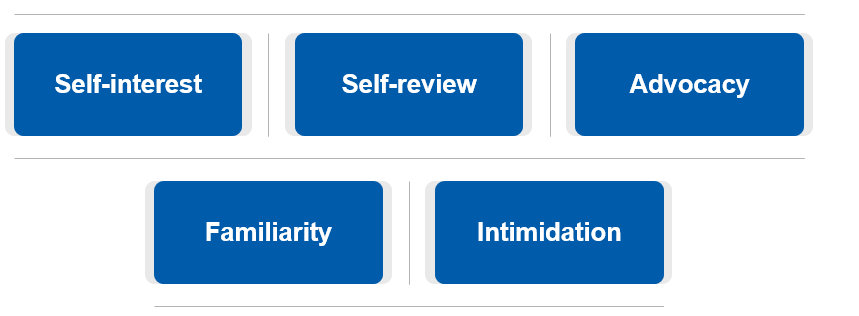

The fundamental principles within the Code – integrity, objectivity, professional competence and due care, confidentiality and professional behavior – establish the standard of behavior expected of a professional accountant (PA) and it reflects the profession’s recognition of its public interest responsibility. Those fundamental principles as well as the categories of threats to them – self-review, self-interest, advocacy, familiarity and intimidation threats are unchanged. Also unchanged, are the overarching requirements to apply the conceptual framework to comply with the fundamental principles and where applicable, be independent. In addition to the structural revisions made to the entire Code, the substantive revisions include:

- An enhanced conceptual framework, which includes extensive revisions to “safeguards” throughout the Code that are better aligned to threats;

- Strengthened independence provisions regarding long association of personnel with audit clients;

- Strengthened provisions relating to offering and accepting of inducements, including gifts and hospitality that apply to both PAs in business (“PAIBs”) and PAs in public practice (“PAPPs”);

- Strengthened provisions dedicated to PAIBs, including:

- A new section relating to pressure to breach the fundamental principles; and

- Revised provisions relating to the preparation and presentation of information.

- Clarifications about the applicability of PAIB provisions to PAPPs;

- New material to emphasize the importance of understanding facts and circumstances when exercising professional judgment; and

- New material to explain how compliance with the fundamental principles supports the exercise of professional skepticism in an audit or other assurance engagements.

An Enhanced Conceptual Framework

|

|

The conceptual framework is a set of principles-based provisions in Section 120, The Conceptual Framework of the Code that all PAs are required to apply to deal with ethics and independence issues. It applies to all PAs and outlines a three-step approach involving identifying, evaluating and addressing threats to compliance with the fundamental principles and, where applicable, independence.

Extensive revisions have been made to the conceptual framework to strengthen and clarify how all PAs are required to identify, evaluate and address threats to the fundamental principles and where applicable, be independent. SMPs should especially take note of the clarifications relating to how PAs should address threats, including the new requirement for PAs to “stand back” and think about whether the overall conclusion made or actions they have taken are appropriate to resolve the issue.

In response to concerns from the regulatory community that some safeguards were not specific or effective enough, the enhanced conceptual framework now includes a more robust definition of safeguards which is “actions, either individually or in combination, that a PA takes that effectively reduce threats to compliance with the fundamental principles to an acceptable level.” It is no longer a valid notion that all threats can be addressed by the application of safeguards. The enhanced conceptual framework clarifies that in certain circumstances, the PA may not have any other option but to decline, or end the specific professional activity, or service.

The enhanced conceptual framework emphasizes that threats are addressed either by eliminating the circumstances creating the threats; applying safeguards where they are available or capable of reducing the identified threats to an acceptable level; or by declining or ending the specific professional activity or service.

In particular, SMPs should note the distinction between safeguards and “conditions, policies and procedures” which are in contrast routine in nature and may assist the PA in identifying and evaluating threats. The conceptual framework clarifies that the conditions, policies and procedures that are established by profession, legislation, regulation, the firm, or the employing organization to enhance PAs acting ethically are not safeguards because they are not specifically designed to deal with a particular threat. Clearer descriptions and definitions of other key terms such as “reasonable and informed third party (RITP)” and “acceptable level” are established, and a new term “appropriate reviewer” was introduced. The Code explains that a RITP test is a concept which involves consideration by a PA about whether the same conclusions would likely be reached by another party (i.e., RITP). The RITP test is made from the perspective of a RITP, and involves weighing all the relevant facts and circumstances that a PA knows, or could reasonably be expected to know, at the time that the conclusions are made. A RITP does not need to be a PA, but should possess relevant knowledge and experience to understand and evaluate the appropriateness of the PA’s conclusions in an impartial manner. The revised description of acceptable level in the enhanced conceptual framework is more closely linked with the concept of RITP test and clarifies that it is the level at which a PA using the RITP test would likely conclude that the PA complies with the fundamental principles.

The enhanced conceptual framework more prominently features the requirement for all PAs to remain alert for new information, or changes to facts and circumstances in applying the conceptual framework. It also explains that once a PA becomes aware of new information or changes to facts and circumstances that might impact whether a threat has been eliminated or reduced to an acceptable level, the PA should evaluate and address that threat accordingly. The enhanced conceptual framework also emphasizes that PAs are required to exercise professional judgment and use the concept of the RITP test in all three stages of applying the conceptual framework.

Finally, the enhanced conceptual framework includes new application material to explain that firms and network firms are to apply the conceptual framework to identify, evaluate and address threats to independence. Responsive to questions about firms’ responsibilities for independence, the Code refers to the International Auditing and Assurance Standards Board’s (IAASB) ISQC 1[1] standard which require firms to establish policies and procedures for complying with independence.

Application of the Conceptual Framework in Relation to Non-Assurance Services

SMPs should take note of the revisions to the independence provisions relating to the provision of non-assurance services (NAS) to audit and assurance clients. Substantive revisions have been made to better explain how firms and network firms are to apply the conceptual framework to deal with independence threats created when NAS are provided to audit and assurance clients.

The prohibitions in the Code relating to NAS are now more prominent, including the overarching prohibition relating to assuming management responsibilities which applies when providing all types of NAS to audit clients. Also, it is now clear which NAS provisions apply in all circumstances; versus which ones apply to audits of entities that are public interest entities (PIEs); and to audits of entities that are not PIEs.

In line with the new description of safeguards in the conceptual framework, the examples of actions that might be safeguards in the NAS section of the Code are much clearer and are more closely aligned to the specific category of threats. The Code clarifies that in some situations, safeguards are not available or capable of reducing the threats that are created by providing NAS to audit clients to an acceptable level, and that if such threats cannot be eliminated, the firm or network firm must decline or end the NAS or the audit engagement.

|

Provision of Recruiting Services to Audit Clients

The Code establishes a new description of recruiting services and clarifies the types of recruiting services that firms and network firms are prohibited from providing to their audit clients. One of those prohibitions relates to searching for, or seeking out candidates and undertaking reference checks of prospective candidates for directors or officers of the entity, and senior management in a position to exert significant influence over the affairs of the clients which is now extended to all entities. It no longer applies to only audits of entities that are PIEs, unlike the extant Code. This is because the IESBA has determined that there are no safeguards available to deal with the familiarity and self-interest threats that are created by providing such recruiting services to audit clients in general.

Long Association

In December 2017, the IESBA finalized changes to its independence provisions relating to long association of personnel with an audit or assurance client, which contain a number of substantive improvements, including a strengthened partner rotation regime for audits of public interest entities. The revised long association provisions were initially drafted in accordance with the structure and drafting conventions of the 2016 edition of the IESBA Code of Ethics for Professional Accountants (“the extant Code”) and is set out in a January 2017 close-off document. Those revisions come into effect in December 2018. In finalizing the revised and restructured Code, restructuring and conforming safeguards-related revisions were made to the long association provisions. However, those revisions did not change the substance of the long association provisions.

|

Also in January 2017, in addition to the related IESBA Staff-prepared Basis for Conclusions document, a Staff-prepared Q&A publication was finalized to assist in the adoption and implementation of the revised long association provisions. This Q&A publication will be updated to align with the paragraph references in the revised and restructured Code and re-issued by December 2018.

Inducements

A few months after the April 2018 release of the revised and restructured Code, the IESBA released revised inducement provisions. Those revised provisions clarify the meaning of inducements, and introduce a more robust and comprehensive framework which clearly delineates the boundaries of acceptable inducements and guides the behaviors of PAIBs and PAPPs in all situations involving inducements. Central to this framework is a new intent test that prohibits the offering or accepting of inducements where there is actual or perceived intent to improperly influence the behavior of the recipient or of another individual. A related Staff-prepared Basis for Conclusions summarizes the rationale for the IESBA’s revisions.

The revised inducement provisions complements the NOCLAR provisions[2] which came into effect in July 2017 and offer a full system of ethical defenses that relate both to malfeasance committed by others and to PAs’ own involvement in potentially unethical behaviors. They represents the last, but no less important piece of the revised and restructured Code and will have the same effective date – June 2019.

Strengthened PAIB Provisions

PAIBs, including those in small- and medium-sized entities (SMEs), play a fundamental role in the financial reporting supply chain and facilitate effective governance in organizations; hence, it is in the public interest that the PAIB provisions in the Code are appropriate and robust. Responsive to stakeholders’ views about areas in the PAIB sections of the Code that should be improved, the IESBA finalized changes to Part C of the extant Code addressing preparation and presentation of information and pressure to breach the fundamental principles. Those changes prohibit PAs from:

- Exercising discretion when preparing or presenting information with an intent to mislead or inappropriately influence contractual or regulatory outcomes and include enhanced application material to assist PAs in disassociating themselves from misleading information.

- Allowing pressure from others to result in a breach of fundamental principles or from placing pressure on others that would lead them to breach fundamental principle. New application material is included with practical examples to help illustrate situations in which PAs may experience pressure to breach the fundamental principles.

The PAIB revisions described above were initially prepared in accordance with the structure and drafting conventions in the extant Code and were finalized in March 2016 (see Revisions to Part C close-off document). In finalizing the revised and restructured Code, the PAIB provisions were further revised to reflect changes arising from the Structure of the Code and Safeguards projects. For example, the PAIBs provisions were clarified to better explain how PAs are to apply the conceptual framework in fulfilling their responsibilities within their respective employer organizations.

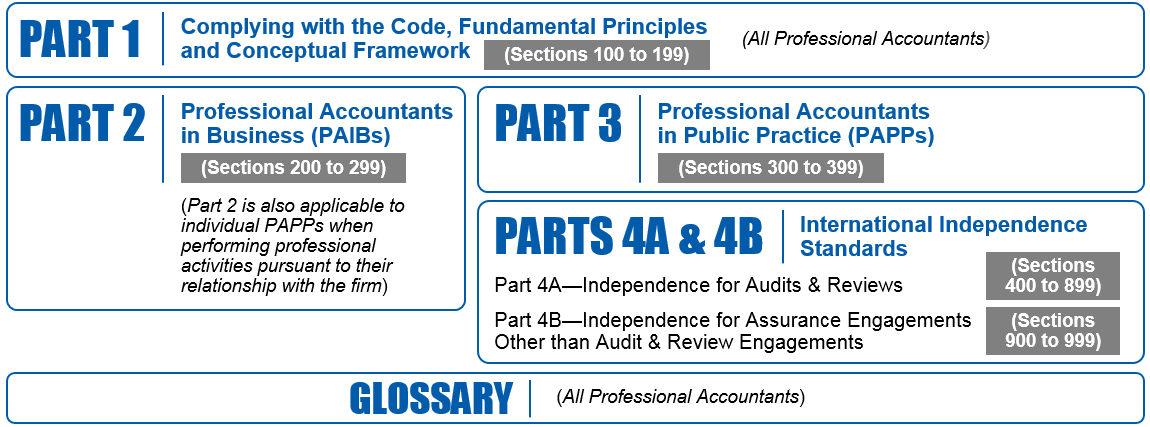

Clarification about Applicability of PAIB Provisions to PAPPs

The IESBA believes that PAPPs – i.e. PAs and firms that provide professional services – might face similar issues and ethical dilemmas as professional PAIBs. Therefore, in finalizing the revised and restructured Code, the IESBA established new requirements and application material to clarify that Part 2[3] of the Code may be relevant to PAPPs when they perform professional activities pursuant to their relationship with the firm, whether as contractors, employees or owners of the firm. SMPs should take note of the various examples that are included in Part 3[4] of the Code to illustrate examples of such situations.

Professional Judgement

In relation to professional judgment, the Code highlights its importance in identifying, evaluating and addressing threats in order to make informed decisions, and to obtain an understanding of specific facts and circumstances, including the nature and scope of the professional activity or service; and the interest and relationship involved. New material has been added to the Code to help PAs better understand what to consider in exercising professional judgment. For example, the Code explains that among other matters, exercising professional judgement involves a consideration of whether:

- There is reason to be concerned that potentially relevant information might be missing from the facts and circumstances known to the PA;

- There is an inconsistency between the known facts and circumstances and the PA’s expectations;

- The PA’s expertise and experience are sufficient to reach a conclusion;

- There is a need to consult with others with relevant expertise or experience;

- The information provides a reasonable basis on which to reach a conclusion;

- The PA’s own preconception or bias might be affecting the accountant’s exercise of professional judgment; and

- There might be other reasonable conclusions that could be reached from the available information.

The new material relating to professional judgment is intended to make more explicit procedures that PAs should already be doing under the extant Code and is expected to ensure that PAs exercise professional judgment in a more consistent manner.

Professional Skepticism

In response to a recommendation from a tripartite Professional Skepticism Working Group (PSWG) comprising representatives of the IAASB, the IESBA and the International Accounting Education Standards Board (IAESB), which was established in 2015, and recognizing the public interest in promoting the application of professional skepticism in audits, reviews and other assurance engagements, the IESBA determined that it would be important to supplement the Code’s existing few references to professional skepticism. The Code now explains how compliance with the fundamental principles supports the exercise of professional skepticism by illustrating this linkage in the context of an audit of financial statements.

In finalizing the material relating to professional skepticism, the IESBA signaled the need for further work to respond to broader concerns identified by some of its stakeholders and the PIOB. In this regard, the IESBA has summarized these issues as well as options for a way forward in a May 2018 Consultation Paper, Professional Skepticism – Meeting Public Expectations (CP). Specifically, the CP explores the behavioral characteristics comprised in the concept of professional skepticism; whether all PAs should be required to apply those behavioral characteristics; and whether, and if so how, the Code should be revised to describe those behaviors.

Restructuring Changes

In addition to the more substantive revisions discussed above, the Code includes several structural revisions that contribute to making it more user friendly. Responsive to stakeholders’ requests to clearly distinguish requirements from application material, requirement paragraphs are identified by the letter “R” and application material that explain those requirements are generally positioned next to them in paragraphs that are identified by the letter “A”.

The language in the Code is now clearer. Where possible, duplicative material is avoided; complex sentence structures are simplified; and passive voice, legalistic and archaic terms are avoided. The Code includes a Glossary with descriptions and definitions of terms which have a specific meaning.

The new structure and drafting convention for the Code establishes a new architecture that emphasizes the Code’s scalability.

|

Guide to the Code

The Code is accompanied by a Guide to the Code to assist readers to better understand its purpose, how the Code is structured, and how to use it. This Guide is non-authoritative and does not form part of the Code itself. SMEs and SMPs are encouraged to familiarize themselves with the Guide as this will certainly help them navigate the various parts and sections of the Code, including the International Independence Standards.

Documentation

The Code carries forward the existing guidance relating to documentation. However, as a form of good practice relating to how they support identifying, evaluating and addressing threats, SMPs may decide that it is helpful to document the details of relevant discussions, actions taken, significant judgments made and conclusions reached.

Adoption and Implementation Support

SMEs and SMPs are encouraged to take action towards implementation now, rather than waiting until June 2019 – the Code’s effective date. The Code is included in the 2018 edition of the IESBA Handbook, which is now available for purchase. A one-stop-shop webpage on the IESBA’s website houses resources and tools to assist in the promotion, adoption and effective implementation of the Code. These resources and tools include:

- A one-pager which summarizes the changes to the Code.

- A series of videos explaining key aspects of the Code.

- A deck of PowerPoint Slides to assist those who wish to deliver presentations about the changes to the Code.

- Five staff-prepared Basis for Conclusions to explain the rationale for the revisions in relation to Structure, Safeguards, Applicability, Professional Skepticism and Professional Judgment, and Inducements.

- A Table of Concordance which compares the paragraphs in the extant Code to those in the revised restructured Code.

- Resources relating to the NOCLAR and Long Association, including related Bases for Conclusion and Staff Q&A documents.

Additional resources and tools, including additional Staff Q&As are being developed and will soon be added. SMEs and SMPs are encouraged to visit the Revised and Restructured Code webpage regularly. Stakeholders, including SMEs and SMPs may request permission (log in required) to reproduce or translate the Code and the related resources and tools.

To Recap

The Code results from the completion of a number of substantive IESBA projects, including the Structure of the Code, Safeguards, and Revision of Part C. It also packages recently completed projects – NOCLAR and Long Association.

Informed by extensive stakeholder engagement over a five year period, the revised and restructured Code is responsive to long-standing concerns about the Code. It also:

- Responds to concerns that the biggest barrier faced by SMPs in complying with the existing Code relates to a lack of a full understanding of its requirements.

- Addresses issues raised by regulators and the PIOB about the robustness of certain provisions in the Code (e.g., safeguards) and its overall enforceability.

- Establishes an integrated set of ethics and independence provisions that are easier to use, navigate and enforce.

The SMP Committee has been actively monitoring the IESBA work on each of the various projects and has engaged with the IESBA often to provide input and suggestions with a focus on matters that impact SME and SMPs constituents.

The SMP Committee notes that the IESBA’s Proposed Strategy and Work Plan for 2019-2023 includes a commitment to promote awareness of the Code and its adoption and effective implementation, including plans to develop an eCode. SMPs are encouraged to remain engaged and provide input to the IESBA’s ongoing initiatives and future projects.

The IESBA plans to introduce a period of stability following the launch of the Code and have committed that no further changes will come into effect before June 2020.

[1] International Standard on Quality Control (ISQC) 1, Quality Control for Firms that Perform Audits and Reviews of Financial Statements and Other Assurance and Related Services Engagements

[2] In finalizing the revised and restructured Code, restructuring changes were made to the NOCLAR provisions. Those changes were not substantive.

[3] Part 2 – Professional Accountants in Business

[4] Part 3 – Professional Accountants in Public Practice