There are six core IFAC activities that support the development, adoption and implementation (A&I) of high-quality international standards.

Image

1) Standards Development & Advocacy

We develop the International Education Standards with the assistance of the International Panel on Accountancy Education and support the development of public sector, audit & assurance and ethics standards by the IPSASB, IAASB and IESBA (the SSBs). This includes providing certain operational and administrative support services.

Leveraging our voice representing our members and the global accountancy profession, we provide extensive feedback on new and revised international standards, primarily to the IAASB and IESBA. This includes formal consultation responses, providing targeted letters on quarterly standard-setting board agendas, and regular targeted meetings on specific projects. It also includes facilitating access to constituency groups, such as IFAC’s Small and Medium Practices and Professional Accountants in Business Advisory Groups, as well as the International Standards Community of Practice.

IFAC Comment Letters

-

Strengthening the Risk-Based Audit Framework: Proposed Revisions to ISA 330, ISA 500, and ISA 520

July 28, 2026 -

Joint Stakeholder Survey: Shaping IAASB and IESBA Strategies for 2028–2031

January 8, 2026 -

Fraud & Going Concern: Revised Standards to Enhance Public Trust

June 17, 2025 -

Embedding Professional Skepticism

March 5, 2024 -

Technology

March 15, 2021 -

ISA for LCE: A Standard for Audits of Less Complex Entities

March 3, 2021 -

Understanding the International Standard on Sustainability Assurance 5000

February 26, 2021 -

Quality Management

May 17, 2019

2) Intellectual Property

The Intellectual Property (IP) department facilitates access to IFAC publications as well as the international standards, supplementary, and non-authoritative publications issued by the SSBs, while simultaneously ensuring they are being properly used and protected through copyright, trademark, and other laws.

To reproduce or translate content issued by IFAC, including standards developed by the SSBs, a permission request is required to be submitted through the online permission request system (OPRI). Access to recently completed or in progress translations are accessible via the Translations Database.

We also facilitate the formatting and publication of SSB Handbooks, pronouncements and other accompanying materials.

3) Awareness Raising

We promote SSB consultations and final pronouncements, as well as adoption and implementation initiatives through our communication channels, including on social media.

We organize events, webinars and outreach covering international standards and involves SSB representatives. This includes organizing new regional IFAC Connect Global Events Series which bring together professional accountancy organizations (PAOs), firms, regulators, standard setters, business and investor communities to address strategic priorities, share intelligence and facilitate key stakeholder collaboration.

4) Targeted Implementation Support

We develop specific materials (e.g., guides, tools, articles and videos) to support the effective and consistent implementation of international standards by professional accountants. We also facilitate access to other resources through the Knowledge Gateway.

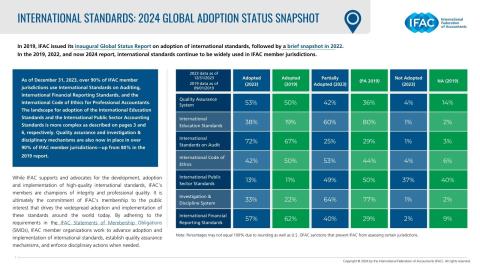

5) Tracking & Reporting Adoption

We track the adoption of international standards. The data comes from the IFAC Member Compliance Program, a longstanding initiative designed to support and elevate accountancy organizations worldwide which all IFAC members must participate in. In joining IFAC, PAOs commit to actions that will advance adoption and implementation of international standards as well as establishing quality assurance and enforcement systems. These commitments are codified in the Statements of Membership Obligations (SMOs). PAOs are required to submit reports (SMO Action Plans) demonstrating how they are progressing with fulfilling the SMOs and any challenges. The SMO Action Plans and information contained in the accompanying IFAC-produced assessments are subsequently published on our website via the International Standards’ Adoption Map.

Image

We produce regular summary publications (see 2024, 2022, 2019 and 2017) which highlight how widely international standards, as well as quality assurance and enforcement systems, are used or in place across IFAC member jurisdictions.

6) Capacity Building

We lead MOSAIC (Memorandum of Understanding to Strengthen Accountancy and Improve Collaboration) to improve cooperation and collaboration between IFAC and the international development community.

We work in collaboration with Development Partners to facilitate access to resources for support and development. IFAC is uniquely positioned to spearhead initiatives that demand global reach, freedom from commercial interests, and the ability to create dialogue and debate.

Through close engagement with our PAOs, we understand specific jurisdiction challenges and coordinate on solutions and targeted initiatives for how these can be addressed. This includes overseeing donor-funded capacity building programs.

We undertake targeted outreach for specific jurisdictions to engage with PAOs, regional organizations and other stakeholders to progress adoption, which often involves support from the PAODAG.