Professional accountants are regularly confronted with ethical choices and moral dilemmas in the course of their professional activities. A recent Australian study sheds light on the persistent ethical conflicts, tensions, and pressures that accountants face when doing their work.

The report provides an overview of the ethical challenges faced by accountants and proposes a set of recommendations for ethics training program design that can enhance accountants’ capabilities in dealing with ethical issues and identifies a list of ethical capability needs across different contexts. Ethical capability is the ability to bridge the gap between actual and desirable professional behaviors and is the most relevant indicator and predictor of ethical behavior in the workplace.

Supported by a national competitive grant from CPA Australia’s Global Research Perspectives Program, a team of academic researchers surveyed and interviewed Australian accounting professionals about:

- the main ethical issues they (or their colleagues) encounter in their professional roles;

- how they (or their colleagues) respond to these ethical issues;

- how their ethical capability to respond could be improved; and

- what resources they need to improve capability.

The study surveyed or interviewed 238 accounting professionals in practice or in business, most of whom are members of CPA Australia and Chartered Accountants Australia & New Zealand.

Key Findings

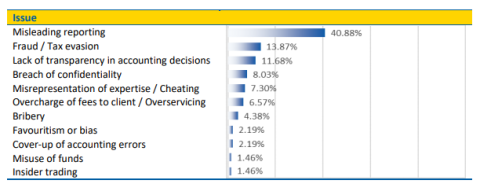

The main ethical issues confronting accounting professionals are:

Table 1: Common Ethical Issues

The actual or potential causes or sources of ethical issues are listed in Table 2, with pressure from clients more prominent than pressure from the employing organization’s management or leadership. Furthermore, when discussing conflicts of interests, respondents expressed concern with systemic problems, inherent in the structure of the organization’s internal accounting policies or performance incentives.

Table 2: Common Causes of Ethical Issues

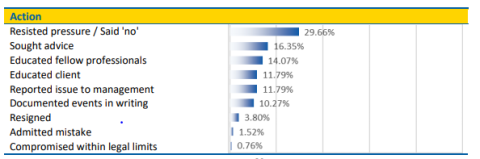

The most common responses to ethical challenges or pressures to act unethically are:

Table 3: Common Responses to Ethical Issues

When considering how ethical issues professional accountants face should be dealt with, the research reveals some key elements for individuals, organizations, and professional accountancy organizations.

For individual professional accountants the key responses are:

- exercise moral courage;

- seek advice from peers;

- report issue to management;

- exercise professional judgment;

- be aware of issue;

- document issue in writing; and

- uphold public interest principle.

In addition, the study summarizes the types of support expected by accountants from their professional organizations, employing organizations, regulators, and government in order to better cope with external pressures on ethical and professional decisions. Although some important expectations were placed on the employer (for example, in terms of upholding accounting standards, building an ethical culture, introducing or improving whistle-blower protection policies and practices, practicing transparency, and applying sanctions), considerably more was expected from professional bodies.

Generally, accountants tend to place a high level of confidence in their professional accountancy organizations, as their role in providing ethics guidance is regarded as considerably more important than the role of government, regulators and, with some qualifications, their own employers. The key areas of support needed from professional bodies to build or enhance ethical capability were education and training, driving social dialogue, building ethical culture within the profession, strengthening advice services, informing and publishing, and resourcing and funding.

One of the main concerns of accounting professionals in this research is the fear of losing objectivity in their judgment due to pressures from clients, employers, or other stakeholders. For many this would be equivalent with de-professionalization or loss of professional identity. Some categories of organizations and individuals are regarded as more vulnerable to loss of objectivity than others. Smaller firms, for example, were seen as experiencing fear of losing clients more intensely. Reasons invoked were lack of information and resources, less experience in how to design internal controls, and increased isolation from opportunities to obtain advice and guidance. Among individual practitioners, young accountants at the beginning of their career were also considered a vulnerable group, as they could be more easily influenced into unethical behavior due to a perceived lack of choice or power.

The ethical capability needs identified in this study can be grouped into three areas.

- Regulation and enforcement needs: improvements in the existing legislation and policies at government and professional levels—such as strengthening whistle-blower protection and simplifying accounting standards, and maintaining ethics breach investigation services.

- Education and training needs: mandatory ethics training; the development of case study banks for experience-based complex ethical situations; the design and delivery of multi-media based ethics training programs; the intensification of associated soft skills training (such as critical thinking, ethical reasoning, communication, and conflict management); and the publication of anonymized real cases of ethical breaches, as well as best ethical practice, with evaluations of ethical issues involved and alternative solutions.

- Advice and mentoring needs: increased availability of professional advice services, maintaining expert ethics hotlines; and coordinating national, state, or local mentoring networks and peer-to-peer resolution groups.

Other policy recommendations include: systemic solutions, openness and transparency in inter-stakeholder communications, peer support, and participation and empowerment.

Overall, research participants clearly indicate that there are many positive attributes of professional accountants and they are generally aware of ethical issues and solutions but are seeking more support, particularly from their professional organizations, to improve ethical capability and ethical practice.

To enhance the entire ethical regime of accountancy, the profession—including practitioners, employing and professional organizations, regulators, and educators—should work more closely together in order to formulate principles and policies that clearly avoid conflicts of interest situations, emphasize highly internalized (and therefore habitual) ethical behaviors in professional accountants’ education and professional development, and design managerial incentives that stimulate such behaviors. A higher level of coordination is required to achieve this, and professional bodies have a key leading role in making it happen.